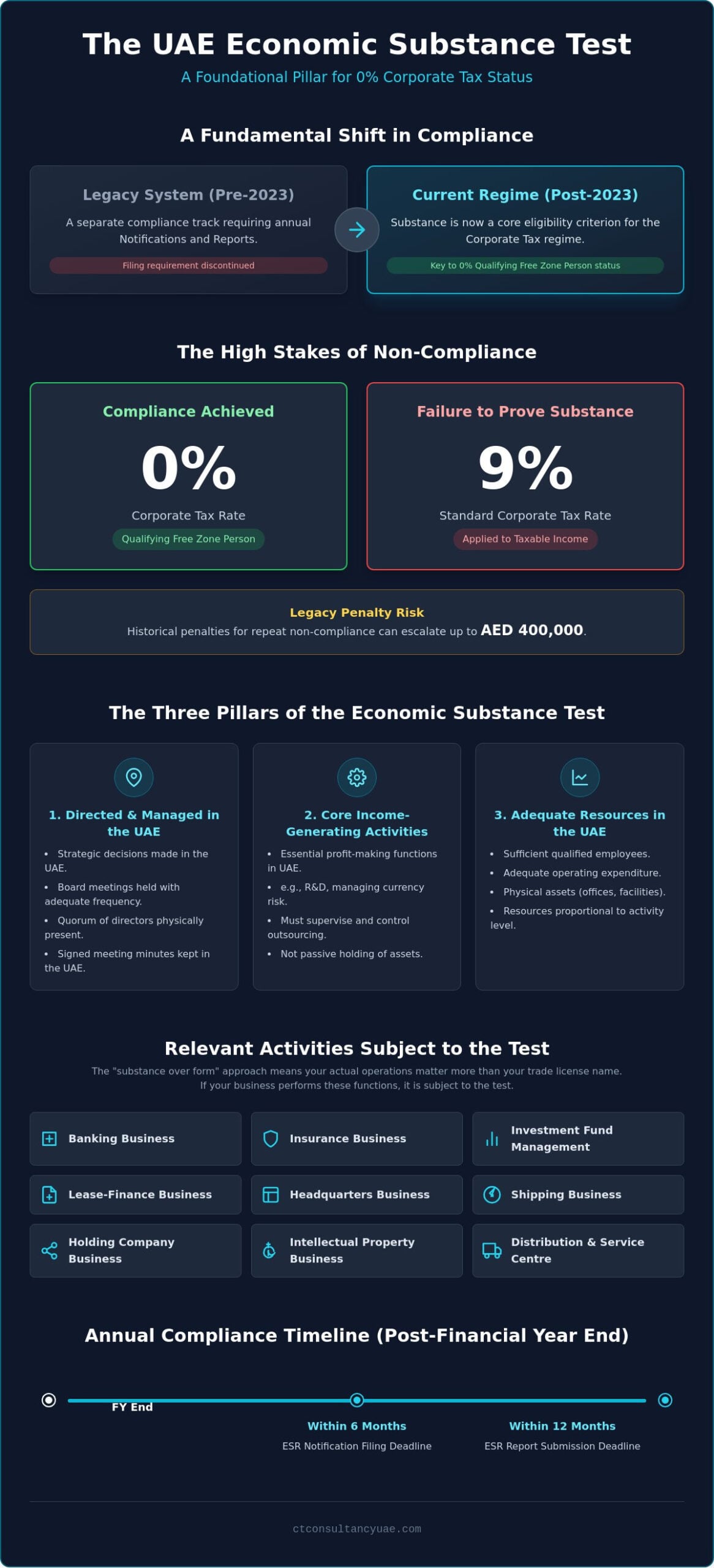

If you believe the discontinuation of separate ESR filings for recent financial years means the economic substance test uae is no longer a priority, you might be risking your company’s 0% tax status. While Cabinet Decision No. 98 of 2024 removed the requirement for new notifications and reports for years starting on or after January 1, 2023, the underlying principle of substance hasn’t disappeared. Instead, it’s become a foundational pillar of the UAE Corporate Tax regime, particularly for those seeking to maintain Qualifying Free Zone Person status. Failing to demonstrate genuine activity now carries the high-stakes risk of being taxed at the standard 9% rate rather than the preferential 0%.

We understand that navigating the intersection of legacy obligations and new tax requirements feels like a moving target. It’s difficult to balance the fear of past penalties, which could escalate to AED 400,000 for repeat non-compliance, with the need for modern corporate governance. This guide provides a definitive roadmap to mastering these complexities. You’ll gain a clear understanding of Core Income Generating Activities (CIGA) and a practical checklist to ensure your business remains fully compliant. We’ll also provide the assurance you need to document “Directed and Managed” criteria with precision, securing your long-term stability in this competitive jurisdiction.

The economic substance test uae serves as a critical regulatory mechanism to verify that entities registered in the Emirates maintain a genuine operational presence proportional to their locally generated income. It’s designed to prevent base erosion and profit shifting, ensuring that profits are taxed where the actual economic activity occurs. While the Ministry of Finance (MoF) remains the competent authority for policy and international reporting, the Federal Tax Authority (FTA) functions as the primary regulatory body responsible for monitoring compliance, conducting audits, and issuing administrative penalties for non-compliance.

As the 2026 corporate tax landscape matures, the principles of substance have transitioned from a standalone reporting requirement to a fundamental eligibility criterion for tax incentives. For companies operating within Free Zones, demonstrating adequate substance is no longer a mere filing formality; it’s the gateway to maintaining Qualifying Free Zone Person (QFZP) status and benefiting from the 0% tax rate. Without meeting these requirements, businesses risk being subjected to the standard 9% corporate tax rate on their entire taxable income. Every licensee must conduct an annual self-assessment to determine if they fall within the threshold of “Relevant Activities,” regardless of whether they’ve historically filed ESR reports.

The UAE regulatory framework utilizes the Economic Substance Doctrine to look beyond the nominal activity listed on a trade license. This “substance over form” approach means that if your actual operations reflect any of the nine core activities, you’re subject to the economic substance test uae. These activities include:

It’s vital to recognize that your trade license name isn’t the final word on compliance. Even if your license specifies “General Trading,” performing the functions of a distribution center for a related party can trigger these obligations. Strategic alignment of your corporate structure is essential, and seeking specialized tax services can help clarify these distinctions before an FTA audit occurs.

To successfully navigate the economic substance test uae, an entity must satisfy three cumulative criteria. These pillars ensure that the business isn’t a “letterbox” company but a functional organization with a physical footprint. While the discontinuation of specific filings for recent years has streamlined administration, the audit focus on these pillars remains intense for Free Zone entities and those remediating past years.

Meeting this requirement involves proving that the strategic decisions of the entity are made within the UAE. It’s not enough to have a local trade license; the board of directors must meet with adequate frequency, and a quorum of these directors must be physically present in the Emirates during those meetings. Every session requires comprehensive minutes that document the strategic discussions and decisions made. These records must be signed and maintained within the jurisdiction. Regulatory authorities look for evidence that directors possess the necessary expertise to perform their fiduciary duties, ensuring that management isn’t merely a rubber-stamp process.

CIGA represents the essential, profit-making activities that a business performs. For a Finance and Leasing business, this might involve agreeing funding terms or managing currency risks. In Intellectual Property (IP) businesses, CIGA focuses on research and development rather than just passive holding. Crucially, while some functions can be outsourced, the CIGA itself must be performed within the UAE. If you utilize third-party providers, you must demonstrate that the entity maintains full supervision and control over the outsourced activities. For those unsure if their current structure holds up to scrutiny, engaging with specialized ESR compliance services can provide the necessary strategic oversight.

The final pillar assesses whether the entity has sufficient resources to conduct its Relevant Activity. This includes having an adequate number of qualified full-time employees (FTEs) residing in the UAE and a physical office space suitable for the business’s scale. Operating expenditure (OPEX) must also be proportionate to the income generated. There’s no one-size-fits-all number; the FTA evaluates “adequacy” based on the specific nature and volume of the company’s operations. Maintaining a local physical office, rather than a flexi-desk or virtual office, remains a stronger indicator of substance during a regulatory review.

While Cabinet Decision No. 98 of 2024 has effectively discontinued the requirement for new Economic Substance Regulations (ESR) notifications and reports for financial years starting on or after January 1, 2023, the economic substance test uae remains a critical retrospective obligation. For the financial years covering 2019 through 2022, the Federal Tax Authority (FTA) continues to exercise its mandate to audit and penalize non-compliance. Understanding the legacy two-step filing process is essential for businesses currently undergoing remediation or addressing outstanding Requests for Information (RFI) from their respective Regulatory Authorities.

The compliance framework originally established a dual-deadline system based on the entity’s financial year-end. A Notification was required within six months of the year-end, serving as a preliminary declaration of whether the entity conducted a Relevant Activity. If an activity was triggered and income was generated, a comprehensive Economic Substance Report was then due within twelve months. This report required granular data on operating expenditure, physical assets, and employee counts. Certain entities, such as investment funds or those owned by the UAE government, could claim “Exempted” status; however, this status still necessitated a formal notification and the submission of supporting evidence to validate the carve-out.

Failure to adhere to these windows for the 2019-2022 period can result in severe financial repercussions, including the AED 400,000 penalty for repeated non-compliance. If your business needs to rectify past filings to safeguard its standing with the FTA, you can secure professional guidance through our Economic Substance Regulations (ESR) Compliance services.

The Ministry of Finance (MoF) digital portal serves as the centralized gateway for all historical ESR submissions. To ensure a successful filing, licensees must upload audited financial statements and detailed board minutes that substantiate the “Directed and Managed” claims discussed in previous sections. A frequent error that triggers regulatory scrutiny is the mismatch between the income reported in the ESR filing and the figures presented in VAT returns or Corporate Tax registrations. Precision in data entry is paramount, as inconsistencies often lead to spontaneous exchanges of information with foreign tax authorities, potentially complicating your global tax position.

The consequences of failing the economic substance test uae extend far beyond the immediate financial burden of administrative fines. While the year-two penalty of AED 400,000 remains a significant deterrent for non-compliance during the 2019-2022 period, the long-term operational risks include the potential suspension or non-renewal of commercial licenses and the spontaneous exchange of sensitive corporate data with international tax authorities. For businesses that identify a deficit in their jurisdictional footprint, strategic remediation must be prioritized before any regulatory audit begins. It’s no longer sufficient to rely on legacy structures that lack a verifiable physical nexus to the Emirates.

Remediation isn’t a retrospective fix but a proactive realignment of your corporate governance. If your entity lacks adequate local presence, you can build substance mid-year by transitioning from virtual office arrangements to dedicated physical spaces or by localizing Core Income Generating Activities (CIGA) through the recruitment of qualified UAE-based personnel. Conducting a pre-emptive ESR compliance audit allows for the identification of these vulnerabilities, providing a structured pathway to satisfy the Federal Tax Authority’s expectations. CTC Tax & Accounting serves as a primary friction-remover in this process, offering the meticulous planning needed to transform compliance from a risk factor into a strategic advantage.

In the current regulatory environment, ESR data cannot exist in a vacuum. It’s imperative to align your substance declarations with your Corporate Tax filings to ensure total consistency across all government submissions. Discrepancies between the income reported for tax purposes and the substance documented for the economic substance test uae can trigger immediate administrative scrutiny. Maintaining this equilibrium requires a sophisticated approach to data management where every CIGA claim is backed by verifiable financial records and logical corporate logic.

Proving the adequacy of operating expenditure relies heavily on the quality of your internal records. Utilizing professional bookkeeping services ensures that every expense, from local utility bills to payroll for UAE residents, is accurately categorized and readily available for audit. These records form the evidentiary trail that demonstrates your business’s genuine economic commitment to the region, providing the final layer of security against regulatory challenges and ensuring your long-term stability in the UAE market.

Mastering the economic substance test uae has evolved from a periodic reporting exercise into a fundamental component of a resilient corporate tax strategy. As we’ve explored, the emphasis has shifted toward maintaining a continuous, verifiable presence that aligns with your broader financial declarations. Success in this landscape requires more than just meeting historical deadlines; it demands a precise synchronization of your board protocols, employee resources, and core profit-making activities within the Emirates. By prioritizing these pillars, you don’t just avoid administrative penalties; you secure the preferential tax status that makes the UAE a premier global business hub.

Navigating these high-stakes requirements doesn’t have to be a source of operational friction. CTC Tax & Accounting offers the specialized authority and regional expertise needed to safeguard your interests. Our advisors bring over a decade of UAE regulatory experience to every engagement, providing end-to-end support that ranges from initial gap analysis to strategic alignment with VAT and Corporate Tax requirements. We ensure that your documentation is meticulous and your substance is beyond reproach.

Secure your business compliance with a professional ESR consultation from CTC Tax & Accounting

With a proactive approach and a dedicated partner, you can transform regulatory complexity into a foundation for stable, frictionless growth in the region.

The test isn’t a universal requirement for every UAE-registered entity. It specifically targets licensees that perform one or more of the nine defined “Relevant Activities,” such as banking, insurance, or distribution and service center business. If your company doesn’t generate income from these specific sectors, the substantive requirements don’t apply. Most firms should still conduct a documented internal assessment to confirm their status; this proactive step prevents accidental non-compliance during future regulatory reviews.

Failing the economic substance test uae triggers a tiered system of administrative penalties and regulatory consequences. For a first-time failure, the Federal Tax Authority may impose a fine of AED 50,000; subsequent failures can escalate to AED 400,000. Beyond financial loss, the authority will spontaneously exchange information with tax officials in the country where the parent company or ultimate beneficial owners reside. This exchange can lead to complex international audits and potential license suspension.

Yes, certain entities are classified as “Exempted Licensees” under the regulatory framework. This category includes investment funds, entities that are tax resident outside the UAE, and companies wholly owned by the UAE government. While these businesses aren’t required to meet the substance pillars, they must still provide sufficient documentary evidence to the Regulatory Authority to validate their exempt status. This process ensures the carve-out is applied accurately while maintaining total transparency with the Ministry of Finance.

Corporate Tax has fundamentally transformed the economic substance test uae from a standalone filing into a prerequisite for tax optimization. To qualify for the 0% rate as a Qualifying Free Zone Person, an entity must demonstrate adequate substance within its respective Free Zone. Failure to meet these criteria results in the application of the standard 9% corporate tax rate. Substance is now the primary mechanism used to verify that profits are legitimately earned within the jurisdiction.

A Notification is a preliminary declaration identifying whether an entity performed a Relevant Activity and generated income during a financial period. In contrast, the Economic Substance Report is a comprehensive filing that provides granular evidence of compliance. The report includes detailed data regarding full-time employees, physical assets, and operating expenditures. While the Notification sets the stage, the Report serves as the definitive proof that the entity satisfies the three pillars of substance during the audit process.