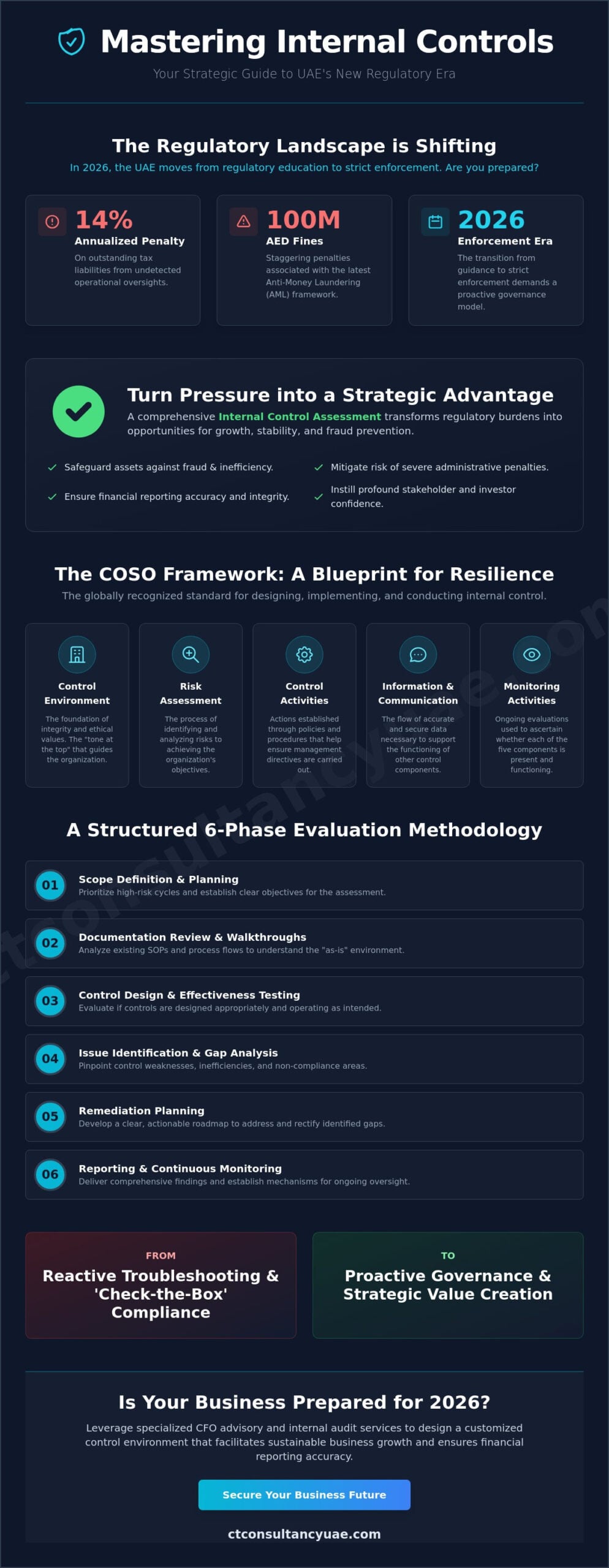

Could your organization withstand a 14% annualized penalty on outstanding tax liabilities simply because a minor operational oversight went undetected? As the UAE transitions from a period of regulatory education to one of active enforcement in 2026, many executives find themselves unsettled by the prospect of FTA audits or the staggering AED 100 million fines associated with the latest anti-money laundering framework. You’ve likely realized that yesterday’s informal processes are no longer sufficient to protect your assets or ensure the accuracy of financial reporting in this maturing market.

By prioritizing a comprehensive internal control assessment, you can transform these regulatory pressures into a strategic advantage that safeguards your business against fraud and inefficiency. This article serves as your executive guide to mastering the complexities of control evaluation, providing a clear roadmap to mitigate risk and drive long-term stability. We’ll examine how to refine your governance structures to meet mandatory audit thresholds and prepare for the upcoming digital shifts in the Emirates’ corporate landscape, ensuring your operations remain frictionless and compliant.

Key Takeaways

- Transition from a reactive to a proactive governance model to navigate the UAE’s maturing regulatory landscape with confidence and strategic precision.

- Establish a robust foundation for financial integrity by conducting a comprehensive internal control assessment based on the globally recognized COSO framework.

- Align your operational safeguards with Federal Tax Authority and Anti-Money Laundering mandates to mitigate the risk of severe administrative penalties and reputational damage.

- Follow a structured, six-phase evaluation methodology that prioritizes meticulous documentation review and precise scoping to identify and rectify hidden operational inefficiencies.

- Leverage specialized CFO advisory and internal audit services to design customized control environments that facilitate sustainable business growth and ensure financial reporting accuracy.

Table of Contents

The Strategic Role of Internal Control Assessment in Corporate Governance

In the maturing financial ecosystem of the Emirates, Internal control is no longer a peripheral administrative task but a cornerstone of executive strategy. An internal control assessment serves as a systematic, objective evaluation designed to verify that a firm’s financial and operational safeguards are functioning as intended. As we enter 2026, the UAE regulatory environment has transitioned from an era of introductory guidance to one of strict enforcement. This shift necessitates a move away from reactive troubleshooting toward a proactive governance model that anticipates risks before they manifest as liabilities.

It’s vital to distinguish between a permanent internal audit function and these periodic, targeted assessments. While an internal audit provides continuous oversight across the entire organization, an internal control assessment is a concentrated “health check” on specific high-risk cycles. This process ensures that your existing SOPs haven’t become obsolete in the face of new mandates, such as the revised AML laws or the latest corporate tax filing requirements. Beyond mere compliance, the primary psychological benefit of this exercise is the instillation of profound stakeholder confidence. When reporting is transparent and backed by verified controls, leadership can operate with a sense of professional calm that’s often missing in high-growth markets.

Mitigating Financial and Operational Risks

A rigorous internal control assessment uncovers hidden vulnerabilities within high-risk areas like cash flow management and procurement cycles. By implementing a strict segregation of duties, businesses can effectively prevent asset misappropriation and internal fraud. These controls do more than just stop leaks; they enhance the fundamental reliability of your financial statements. For companies seeking bank financing or preparing for a business valuation, having verified, accurate data is the ultimate differentiator that streamlines the due diligence process and secures favorable terms.

Establishing Professional Authority through Governance

True governance begins when the board and senior management establish a clear “tone at the top,” signaling that integrity is non-negotiable. Robust controls demonstrate a level of corporate maturity that attracts sophisticated investors and high-tier partners. We’ve moved past the days of “check-the-box” compliance. In 2026, sophisticated internal controls are viewed as tools for strategic value creation. Leveraging CFO advisory services ensures that your control architecture is not just compliant, but optimized for growth, ensuring every financial report is backed by a verifiable chain of logic and accountability.

Core Components of a Modern Internal Control Framework

Designing a resilient business requires more than just high-level oversight; it demands a structured methodology. Most elite consultants utilize the COSO framework as the gold standard for any internal control assessment. This framework provides a comprehensive lens through which we evaluate five critical areas: the control environment, risk assessment, control activities, information and communication, and monitoring activities. Without this structured approach, an evaluation remains superficial, failing to capture the nuanced vulnerabilities that often lead to financial misstatement or regulatory friction.

The control environment acts as the foundation of this entire structure. It encompasses the organizational culture, ethical values, and the competence of your personnel. If the “tone at the top” doesn’t prioritize integrity, even the most sophisticated software won’t prevent systemic failures. Similarly, information and communication channels must be robust to ensure data integrity across departments. In 2026, the speed of commerce in Dubai and Abu Dhabi means that information must flow accurately and securely. It’s a legacy approach to rely solely on annual checks. Modern resilience is built on continuous monitoring, where anomalies are flagged in real-time rather than discovered during a stressful year-end audit.

Risk Assessment and Control Activities

Effective risk assessment starts with identifying specific operational objectives and analyzing the potential hurdles to achieving them. Once these risks are mapped, we implement a mix of preventive and detective controls. Preventive controls, such as strict authorization limits, stop errors before they happen. Detective controls, like monthly bank reconciliations, identify issues after the fact. Documenting these processes into clear Standard Operating Procedures (SOPs) is essential, as seen in sectors like real estate where 360 Apartment Renovations uses standardized workflows to maintain control during rapid unit turnovers. These documents serve as the benchmarks for your team and provide the clarity needed for a successful internal control assessment.

Information Systems and Data Integrity

Modern accounting software plays a pivotal role in automating control points. By reducing manual entry, you significantly lower the risk of human error and unauthorized manipulation. However, automation requires its own set of safeguards. Securing financial data through multi-factor authentication and role-based access is non-negotiable. A robust “audit trail” must be maintained, ensuring that every transaction can be traced back to its origin for external verification. If you’re unsure if your current systems meet these standards, engaging with CFO advisory services can help you design a digital infrastructure that supports both compliance and scale.

Navigating UAE Compliance: Aligning Controls with Tax and AML Mandates

A common misconception among SME owners is that smaller operational scales offer a shield against regulatory scrutiny. In the 2026 UAE business environment, this assumption is not only inaccurate but potentially devastating. The Federal Tax Authority (FTA) and other regulatory bodies have shifted focus toward active enforcement, making a rigorous internal control assessment a necessity for businesses of all sizes. Whether you’re managing a local startup or a branch of a multinational, your internal controls serve as the primary defense against the 14% annualized late payment penalties established under Cabinet Decision No. 129 of 2025.

Your internal controls must be meticulously aligned with the 9% corporate tax regime. Without formalized tracking, identifying every deductible expense becomes an exercise in guesswork, leading to financial misstatements that trigger audits. Similarly, maintaining compliance with Economic Substance Regulations (ESR) requires more than just a yearly filing; it demands a continuous, documented flow of operational data that proves your business’s core income-generating activities are conducted within the Emirates. An internal control assessment ensures these tracking mechanisms are embedded into your daily workflow, preventing the friction of last-minute data reconstruction.

Corporate Tax and VAT Readiness

Effective tax planning relies on the integrity of your underlying data. By implementing controls that capture and categorize every transaction, you provide the necessary evidence for Corporate Tax Consultants Dubai to optimize your tax position. This level of precision is equally critical for VAT. Regular reconciliations between input and output tax are essential to avoid the steep administrative penalties associated with incorrect filings. Ultimately, professional VAT registration services in the UAE are only as effective as the internal data they receive, making robust controls the linchpin of your tax strategy.

AML Compliance and UBO Reporting

The stakes for non-compliance have reached an all-time high with Federal Decree-Law No. 10 of 2025, which can impose fines of up to AED 100 million on legal entities. Your internal framework must include robust Know Your Customer (KYC) protocols and systematic reviews of Ultimate Beneficial Ownership (UBO) status. These aren’t just one-off tasks. They’re ongoing control activities that must be monitored to reflect real-time changes in ownership or risk profiles. In a landscape where regulators value demonstrable governance over “on-paper” compliance, having an audited trail of these reviews is your best protection against severe administrative sanctions.

A Professional 6-Step Methodology for Internal Control Evaluation

Executing a robust internal control assessment requires methodological rigor rather than a fragmented approach. By following a structured six-phase evaluation, leadership can move from uncertainty to a state of verified resilience. This process begins with Planning and Scoping, where we define the boundaries of the assessment by identifying high-risk financial cycles. For instance, given the FTA requirement to maintain records for seven years, scoping must ensure that data retention protocols are sufficiently durable. We then move to Documentation Review, where existing SOPs and flowcharts are analyzed to see if they align with current UAE mandates.

The third phase involves the Testing of Controls through detailed walkthroughs and sample testing. This leads directly into Gap Analysis, where we identify deficiencies or material weaknesses that could lead to financial misstatement. Once gaps are identified, we initiate Remediation Planning, developing a prioritized roadmap for control improvement. The cycle concludes with Final Reporting, where findings are presented to executive leadership with clear, actionable recommendations. This structured progression ensures that no vulnerability remains unaddressed, providing a frictionless path toward total compliance.

Testing and Validating Effectiveness

Testing is the most critical phase of the internal control assessment. We utilize three primary methods: observation of live processes, inspection of physical or digital records, and re-performance of the control itself. It’s essential to distinguish between design effectiveness, which asks if the control is built correctly, and operating effectiveness, which asks if the control is actually followed in practice. Every “exception” found during testing is documented to determine its root cause, ensuring that we aren’t just treating symptoms but fixing systemic flaws. If your current records lack this level of detail, integrating professional bookkeeping and accounting services can provide the necessary data foundation for valid testing.

Remediation and Continuous Improvement

Remediation isn’t about fixing everything at once; it’s about prioritizing gaps based on your organization’s specific risk appetite and the potential financial impact. We assign clear ownership for each improvement to specific department heads to ensure accountability. A timeline for follow-up assessments is established to verify that the remediated controls are functioning as intended. This commitment to continuous improvement transforms the assessment from a one-time event into a permanent strategic asset that evolves alongside the UAE’s regulatory landscape.

Leveraging Strategic CFO Advisory and Internal Audit Services

Establishing a robust internal control framework is the non-negotiable first step toward Strategic Financial Management for SMEs. Without this foundation, financial data remains suspect, and strategic planning becomes a gamble rather than a calculated exercise in growth. A comprehensive internal control assessment provides the baseline intelligence required to move from basic survival to sophisticated financial leadership. In the 2026 UAE market, where the margin for error has been narrowed by strict enforcement, this assessment isn’t merely a compliance hurdle; it’s the data bedrock upon which all future expansion is built.

Utilizing specialized CFO Advisory Services Dubai allows business owners to outsource the complex design and implementation of these controls. This partnership transforms the finance function from a cost center into a strategic asset, ensuring that every operational safeguard is aligned with the firm’s overarching commercial goals. Once the initial evaluation is complete, many organizations choose to transition to a permanent internal audit function. This shift ensures that the precision established during the assessment is maintained, providing a frictionless journey through the Emirates’ evolving tax and legal landscapes.

The Value of an Independent Perspective

Internal teams, while deeply knowledgeable about daily operations, often develop blind spots to subtle control deficiencies. Familiarity can lead to a relaxation of protocols, which is why an independent, third-party internal control assessment is so vital. External experts bring a level of objectivity and regional regulatory expertise that internal staff simply cannot replicate. These independent reports provide a significant credibility boost when dealing with investors or financial institutions. Moreover, the findings from a professional assessment serve to streamline the annual external audit process, reducing the time and resources required to satisfy mandatory corporate tax audit thresholds for companies exceeding the AED 50 million revenue mark.

Driving Growth through Controlled Environments

Strong controls don’t hinder speed; they enable it. When a business operates within a controlled environment, leadership can scale operations with the confidence that the underlying systems are resilient enough to handle increased volume. By automating routine control points within your accounting software, you significantly reduce the “cost of compliance” and free up your team to focus on value-added activities. CTC Tax & Accounting provides the meticulous planning and expert oversight needed to turn these regulatory requirements into competitive advantages. To begin fortifying your organization’s resilience, consider booking a comprehensive Business Advisory consultation to identify your specific risk profile and growth opportunities.

Fortifying Your Operational Foundation for 2026 and Beyond

The transition from a period of regulatory education to one of active enforcement in the Emirates necessitates a fundamental shift in how organizations perceive their governance structures. As we’ve explored, a modern framework must seamlessly integrate with Corporate Tax and AML mandates while utilizing a structured methodology to identify material weaknesses. By conducting a rigorous internal control assessment, you don’t just avoid penalties; you build a resilient platform for sustainable, confident scaling.

At CTC Tax & Accounting, we bring over a decade of UAE regulatory expertise to every engagement, offering a specialized focus on SME growth and comprehensive CFO and Audit advisory services under one roof. Our team acts as your primary friction-remover, navigating the nuances of the local landscape to ensure your business remains secure and efficient. Secure your business today with a professional Internal Control Assessment from CTC Tax & Accounting.

It’s time to replace operational anxiety with strategic precision. With the right controls in place, your organization is prepared to thrive in the maturing UAE market.

Frequently Asked Questions

What is the primary objective of an internal control assessment?

The primary objective is to provide reasonable assurance that an organization’s operational, reporting, and compliance goals are achieved. It focuses on safeguarding assets against loss or unauthorized use while ensuring that financial statements are prepared with a high degree of reliability. By systematically evaluating these safeguards, management can identify vulnerabilities before they manifest as costly financial or legal liabilities.

How often should a UAE company evaluate its internal controls?

A UAE company should ideally perform an internal control assessment at least once per year to align with the standard financial reporting cycle. However, more frequent evaluations are necessary when significant changes occur, such as the implementation of mandatory e-invoicing pilot programs in July 2026. Proactive monitoring ensures that your governance framework remains resilient against evolving administrative penalties and operational shifts.

Who is responsible for the internal control system within a business?

The Board of Directors and senior management hold the ultimate responsibility for establishing and maintaining an effective internal control system. While day-to-day execution is delegated to department heads and staff, leadership must set the “tone at the top” to prioritize integrity and ethical values. This accountability ensures that the control environment is integrated into the firm’s strategic objectives rather than being treated as a secondary administrative task.

Can internal controls completely eliminate the risk of fraud?

No system of controls can completely eliminate the risk of fraud, as they are designed to provide reasonable rather than absolute assurance. Even a robust framework can be circumvented through sophisticated collusion among employees or the deliberate override of protocols by management. However, a well-designed system significantly increases the likelihood of detection and serves as a powerful deterrent against misappropriation and financial misstatement.

What are the three main types of internal controls?

The three primary types are preventive, detective, and corrective controls. Preventive controls, such as the segregation of duties and authorization limits, aim to stop errors or fraud before they occur. Detective controls, like monthly bank reconciliations, identify anomalies after a transaction has taken place. Corrective controls are the procedures utilized to rectify the root causes of identified issues, ensuring the organization prevents recurrence.

How does an internal control assessment differ from an external audit?

An internal control assessment is a proactive, management-driven evaluation focused on operational efficiency and risk mitigation, whereas an external audit is a statutory requirement focused on the fairness of financial statements. While an external auditor examines controls to determine the extent of their testing, the internal assessment goes deeper into governance and strategic alignment. This internal focus helps prepare the organization for the rigors of external scrutiny.

Is an internal control assessment mandatory for UAE mainland companies?

While not universally mandatory for every small mainland business, an assessment is effectively required for companies with revenue exceeding AED 50 million to support mandatory corporate tax audits. Additionally, Qualifying Free Zone Persons must maintain audited financial statements to benefit from the 0% tax rate. Even when not legally compelled, professional advisors recommend these evaluations to mitigate the risk of staggering AML fines and FTA penalties.

What are the consequences of having weak internal controls in the UAE?

Weak internal controls can lead to severe legal repercussions, including administrative fines of up to AED 100 million under the 2025 AML framework. Businesses also face a 14% annualized penalty on outstanding tax amounts due to late payments or filing errors. Beyond financial loss, the reputational damage and potential loss of commercial licenses can permanently disrupt an organization’s ability to operate within the Emirates.