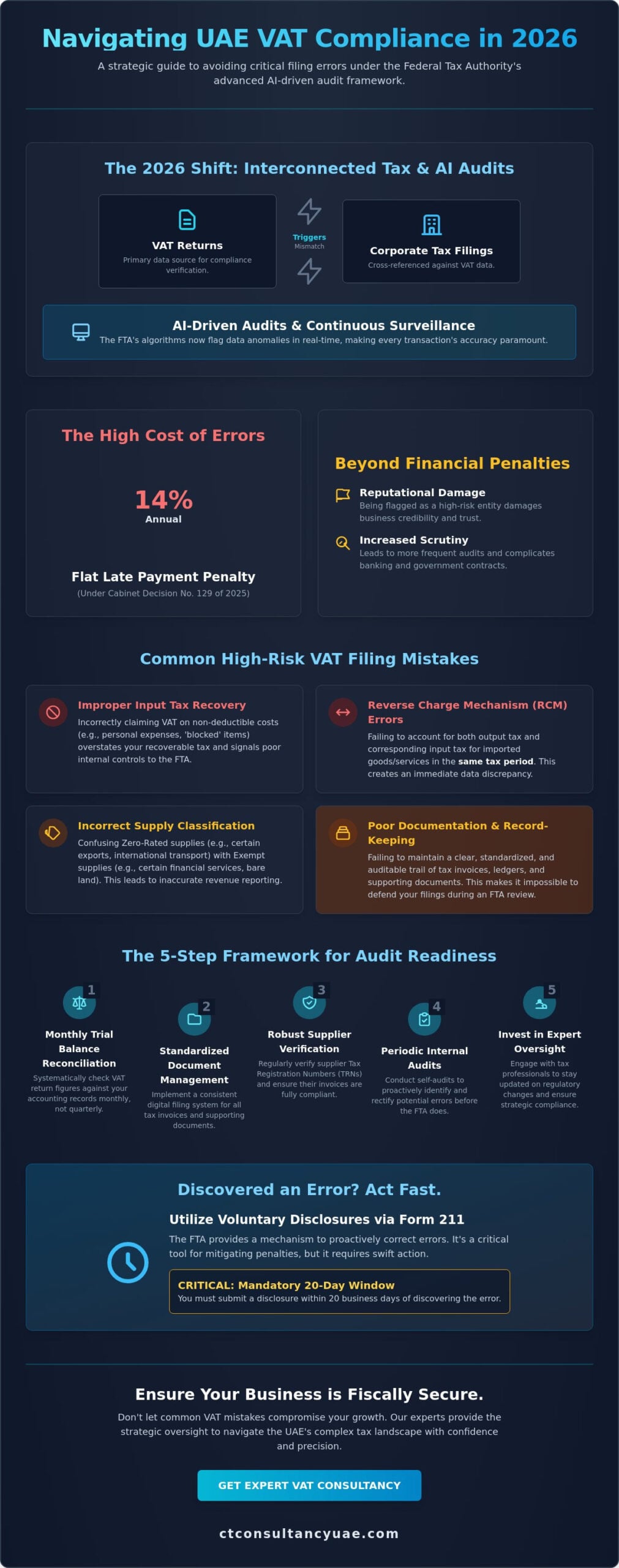

In 2026, a single data mismatch in your tax return is no longer just a clerical error; it’s the primary catalyst for comprehensive multi-tax audits by the Federal Tax Authority. You’ve likely felt the increasing pressure of the UAE’s evolving regulatory framework, especially with the recent implementation of Cabinet Decision No. 129 of 2025 and its reformed penalty structures. It’s natural to feel concerned about the flat 14% annual late payment penalty or the complexities of the updated reverse charge mechanism. We understand that identifying and avoiding common VAT filing mistakes in the UAE businesses make is essential for maintaining a frictionless corporate presence.

This guide provides the strategic oversight needed to rectify frequent errors before they escalate into significant financial liabilities. By addressing these high-risk areas, you’ll gain the confidence to manage your tax profile with the same rigor you apply to your core growth strategies. We’ll examine critical issues like input tax recovery and supplier verification while establishing a robust framework for internal audit readiness that ensures your long-term fiscal security.

Key Takeaways

- Understand the critical synergy between VAT data and Corporate Tax submissions within the 2026 UAE regulatory framework.

- Identify and rectify common VAT filing mistakes in the UAE businesses encounter regarding Input Tax recovery and Reverse Charge Mechanism (RCM) complexities.

- Master the essential distinctions between Zero-Rated and Exempt supplies to ensure precise revenue classification and Article 59 invoice compliance.

- Implement a structured five-step framework for monthly trial balance reconciliation and standardized document management to mitigate audit risks.

- Learn the strategic application of Voluntary Disclosures via Form 211 and the mandatory 20-day window for correcting discovered discrepancies.

Table of Contents

The Evolving Landscape of VAT Compliance in the UAE

The regulatory environment in 2026 reflects a sophisticated tax regime that demands absolute precision from every registrant. Since the introduction of Taxation in the United Arab Emirates, the Federal Tax Authority (FTA) has transitioned from a period of educational leniency to one of rigorous enforcement. VAT filing is no longer merely a quarterly administrative task; it’s the primary data source that the FTA uses to cross-reference with Corporate Tax submissions. Any discrepancy between your VAT returns and your Corporate Tax declarations now serves as a high-probability trigger for an investigation. This interconnectedness means that common VAT filing mistakes in the UAE businesses once considered minor can now lead to systemic tax challenges across multiple fiscal obligations. The FTA has deployed advanced AI-driven audit tools that flag anomalies in real-time, moving away from manual oversight toward a model of continuous digital surveillance. These algorithms are designed to identify patterns of non-compliance that human auditors might overlook, making the accuracy of every transaction paramount.

The Cost of Non-Compliance: Beyond Financial Penalties

Administrative penalties represent an immediate drain on corporate liquidity. Under Cabinet Decision No. 129 of 2025, the late payment penalty is established as a flat 14% annual rate, calculated monthly. While these financial repercussions are significant, the long-term reputational damage of being flagged as a high-risk entity is often more detrimental. Such a designation can lead to increased scrutiny in future periods and complicate standard business processes, including banking relationships and government contract bidding. A tax audit is a comprehensive review of all financial records, including purchase invoices, sales ledgers, and bank statements, to verify the accuracy of reported figures. Entities that don’t consistently maintain high standards find their operational focus diverted from growth to defensive accounting.

Why 2026 is a Critical Year for UAE Taxpayers

The maturity of the UAE tax system has ushered in an era of “tax digitality,” where the FTA expects seamless integration between business accounting software and tax reporting portals. In 2026, the focus has shifted toward supplier verification and the integrity of the digital trail. Maintaining a high standard of VAT Registration and Compliance is essential for any enterprise seeking to avoid the scrutiny of automated audit algorithms. Precision in common VAT filing mistakes in the UAE prevention is the only way to ensure that your business remains fiscally secure in this high-stakes environment. As the system continues to evolve, the businesses that thrive will be those that view tax compliance as a strategic pillar rather than a mere regulatory hurdle.

Technical precision serves as the cornerstone of fiscal stability in a mature tax environment. Among the common VAT filing mistakes in the UAE entities frequently encounter, the improper recovery of input tax remains the most persistent and scrutinized. This often stems from a fundamental misunderstanding of which expenses qualify for deduction under the Official UAE VAT General Guide. While businesses are entitled to reclaim VAT on costs incurred for making taxable supplies, the distinction between deductible business expenses and non-deductible personal or ‘blocked’ costs is frequently blurred in practice. Failing to distinguish between these categories doesn’t just result in an overstatement of credit; it signals a lack of internal controls to the Federal Tax Authority.

Mastering the Reverse Charge Mechanism (RCM)

The Reverse Charge Mechanism represents a significant area of risk for businesses importing services or goods from abroad. Under the RCM, the responsibility to account for VAT shifts from the foreign supplier to the UAE-based recipient. A frequent oversight involves failing to report both the output tax and the corresponding input tax within the same tax period. This omission creates an immediate imbalance in the digital records held by the FTA. Although Federal Decree-Law No. (16) of 2025 has simplified some documentation requirements, businesses must still ensure that cross-border transactions are meticulously recorded to maintain audit readiness. It’s vital to reconcile these imports with customs data to ensure every transaction is captured in the correct return.

Blocked Input Tax: The Hidden Compliance Trap

Certain expenditures are explicitly ‘blocked’ from tax recovery, regardless of their perceived connection to business activities. Entertainment services, which include hospitality, food, and accommodation provided to anyone who is not an employee, are generally non-recoverable. Similarly, VAT on the purchase, lease, or repair of motor vehicles available for private use cannot be reclaimed. These nuances are often the first points of inspection during an FTA review. Engaging in a periodic VAT compliance review allows leadership to identify these hidden traps before they manifest as administrative penalties. We recommend that executives implement a strict classification policy for all hospitality and transport-related costs to ensure only eligible tax is recovered. Securing expert tax advisory is often the most effective way to navigate these high-stakes technicalities without disrupting operational momentum.

Administrative Oversights: Documentation and Classification

While technical errors like the Reverse Charge Mechanism are complex, administrative oversights are among the most common VAT filing mistakes in the UAE businesses commit, often due to a lack of procedural discipline. These errors frequently involve the fundamental misclassification of supplies or the failure to maintain a robust document trail that satisfies the Federal Tax Authority (FTA). Beyond technical accuracy, the FTA expects a meticulous archival system where every transaction is supported by a valid tax invoice. Another frequent administrative pitfall is the use of incorrect exchange rates for non-AED invoices. The law requires that all foreign currency amounts be converted using the specific daily rates published by the UAE Central Bank. Relying on commercial bank rates or internal accounting software defaults creates discrepancies that can lead to significant reconciliation issues during an audit.

Zero-Rated vs. Exempt: A Strategic Distinction

One critical area of confusion involves the distinction between zero-rated and exempt supplies. While neither category results in a 5% tax charge to the customer, their impact on your business’s fiscal health is vastly different. Zero-rated supplies are taxed at 0%, which allows the business to recover input tax on related expenses. In contrast, exempt supplies don’t allow for any input tax recovery. For diversified businesses, this creates the challenge of “Partial Exemption,” where input tax must be apportioned between taxable and exempt activities. Misclassifying an exempt supply as zero-rated leads to the illegal recovery of input tax, a mistake that often necessitates a voluntary disclosure, as noted in expert commentary by KPMG on Correcting VAT Errors. Precision in this classification is the only way to safeguard your right to tax recovery.

The Anatomy of a Compliant UAE Tax Invoice

Article 59 of the UAE Executive Regulations defines the specific requirements for a valid tax invoice. Every document must include the supplier’s Tax Registration Number (TRN), a unique sequential number, the date of issue, and a clear breakdown of the VAT amount in AED. A frequent error is the issuance of ‘Proforma’ invoices as final tax documents; these aren’t recognized for tax recovery purposes and will be rejected during an audit. Maintaining these records for the mandatory five-year period (or 15 years for real estate) is a non-negotiable requirement. Integrating professional Bookkeeping and Accounting Services ensures that your invoicing workflow is compliant from the point of sale, preventing common VAT filing mistakes in the UAE from entering your permanent financial records. It’s much simpler to establish a compliant system today than to reconstruct years of documentation under the pressure of an active FTA investigation.

The 5-Step Framework to Eliminate VAT Filing Errors

In the current fiscal climate, VAT data is no longer siloed; it serves as a foundational component of your Corporate Tax profile. Discrepancies identified in VAT returns can trigger audits that extend into your Corporate Tax filings, making accuracy a multi-dimensional requirement. Adopting a structured methodology is the most effective way to prevent common VAT filing mistakes in the UAE businesses often overlook during routine processing. This framework ensures that your tax data remains consistent across all regulatory submissions, providing a shield against the Federal Tax Authority’s automated surveillance systems.

To achieve long-term fiscal security, we recommend the following five-step protocol:

- Perform monthly reconciliations between the trial balance and the VAT return to identify ledger anomalies.

- Establish a centralized digital repository for all tax invoices to ensure immediate accessibility during an audit.

- Conduct periodic internal VAT health checks to verify the classification of zero-rated and exempt supplies.

- Configure accounting software with UAE-specific VAT codes to automate the calculation of recoverable tax.

- Appoint an external compliance partner to provide an objective final review before submission.

Reconciliation: The Foundation of Accuracy

Accuracy begins with a rigorous comparison between the general ledger and the tax return. Output VAT must be meticulously matched to the total sales recorded in the ledger, ensuring every taxable transaction is accounted for. Simultaneously, Input VAT requires verification against physical purchase invoices to confirm that only eligible, non-blocked tax is recovered. Discrepancies often arise from timing differences or missed credit notes, which can be easily rectified if caught early. Utilizing professional Internal Audit Services provides an objective layer of scrutiny that identifies these reconciliation gaps before they reach the FTA. This proactive approach transforms compliance from a reactive burden into a controlled business process.

Software Configuration and Digital Records

Transitioning from manual spreadsheets to automated accounting systems is no longer optional in a digital-first regulatory environment. Real-time data entry prevents the errors inherent in month-end filing rushes, allowing for continuous oversight of your tax position. Your software must be precisely configured to handle the nuances of the UAE tax code, including the proper treatment of the Reverse Charge Mechanism for imported services. Integrating CFO Advisory Services can help align these technical setups with your broader financial objectives, ensuring your technology facilitates seamless reporting rather than creating data silos. By digitizing your records, you ensure that every claim is backed by a compliant document trail, significantly reducing the risk of common VAT filing mistakes in the UAE enterprises face during formal inspections. Securing VAT Registration and Compliance support is a vital step in validating that your software logic remains updated with the latest 2026 regulations.

Strategic Remedies: Voluntary Disclosures and Expert Oversight

Even the most meticulous enterprises may occasionally uncover historical discrepancies in their tax records. In the 2026 regulatory environment, the discovery of common VAT filing mistakes in the UAE registrants make doesn’t have to result in catastrophic penalties if managed with strategic foresight. The Federal Tax Authority provides a formal mechanism known as Voluntary Disclosure, submitted via Form 211, to rectify these inaccuracies. This process is more than a simple correction; it’s a proactive demonstration of compliance that can significantly mitigate financial exposure. By choosing to self-correct, a business signals its commitment to transparency, which is vital for maintaining a low-risk profile in the FTA’s digital surveillance systems.

Timing is the most critical factor when managing a Voluntary Disclosure. UAE law mandates that once an error is discovered, the taxpayer has exactly 20 business days to submit the disclosure to the FTA. Delaying this submission beyond the 20-day window can lead to additional administrative penalties, compounding the original error. Deciding whether a VD is mandatory or a strategic choice often depends on the net tax impact. While minor errors might occasionally be adjusted in a subsequent return, any mistake resulting in a significant tax difference generally requires a formal disclosure to maintain a clean compliance record and avoid the 15% fixed penalty associated with FTA-discovered errors.

Navigating the Voluntary Disclosure Process

Submitting a Form 211 requires a precise calculation of the tax difference across all affected periods. This task is complicated by the fact that one error often creates a ripple effect throughout the ledger, impacting subsequent returns and potentially your Corporate Tax liabilities. By filing a VD before an audit notification is received, businesses benefit from a significantly reduced penalty structure. Under current 2026 regulations, voluntary disclosures are subject to a 1% monthly penalty on the tax difference from the original due date, which is far less punitive than the penalties triggered during an active FTA investigation. Securing professional VAT Registration and Compliance support is essential to ensure that the disclosure is comprehensive and leaves no room for further inquiry.

The Value of a Strategic Tax Partner

CTC Tax & Accounting serves as the primary friction-remover for businesses operating in the UAE’s high-stakes regulatory landscape. Our approach transcends basic filing; we provide a partnership rooted in precision and long-term stability. By integrating CFO Advisory Services into your tax strategy, we help you transition from reactive error correction to proactive fiscal planning. This high-level oversight ensures that your business remains resilient against the evolving requirements of the UAE tax landscape. We invite you to contact our consultants to conduct a thorough review of your current filings and secure your 2026 tax position with the expertise your enterprise deserves.

Fortifying Your Compliance Infrastructure for 2026

The transition toward a more mature and digitally integrated tax system in the UAE necessitates a shift from reactive accounting to proactive fiscal governance. By mastering the nuances of the Reverse Charge Mechanism and establishing rigorous documentation standards, you effectively eliminate the common VAT filing mistakes in the UAE businesses often encounter under the scrutiny of the Federal Tax Authority. Implementing a structured reconciliation framework ensures that your VAT data remains a reliable foundation for your broader Corporate Tax profile, safeguarding your enterprise against the financial and reputational risks of non-compliance.

At CTC Tax & Accounting, we leverage decades of international financial expertise and specialized UAE regulatory knowledge to provide end-to-end, stress-free compliance solutions tailored to your unique operational needs. Our team acts as your strategic partner, removing regulatory friction so you can focus on sustainable growth. Secure your business with expert VAT compliance from CTC Tax & Accounting. We’re here to ensure your journey in the UAE market remains secure and prosperous.

Frequently Asked Questions

What is the penalty for late VAT filing in the UAE in 2026?

The administrative penalty for failing to submit a VAT return within the specified timeframe is AED 1,000 for the first offense, increasing to AED 2,000 for repeated violations within a 24-month period. Additionally, late payments are subject to a flat 14% annual interest rate, calculated monthly on the outstanding balance. These costs represent an unnecessary drain on corporate liquidity that businesses can avoid through disciplined filing schedules and professional oversight.

Can I correct a VAT return after it has been submitted to the FTA?

You can rectify submitted returns by utilizing the Voluntary Disclosure (Form 211) mechanism or by making adjustments in the subsequent tax return if the tax difference is less than AED 10,000. If the error exceeds this threshold, a formal disclosure is required within 20 business days of discovery. Addressing common VAT filing mistakes in the UAE registrants uncover through these channels is essential for maintaining a clean compliance record with the Federal Tax Authority.

Is a Voluntary Disclosure mandatory for all VAT errors?

A Voluntary Disclosure is only mandatory if the discovered error results in a tax difference exceeding AED 10,000. For discrepancies below this amount, the law allows for a correction in the next tax period’s return. However, choosing to file a disclosure strategically, even for smaller amounts, can be beneficial if an audit is imminent, as it demonstrates proactive transparency and can mitigate the risk of more severe penalties during an inspection.

What are the most common reasons for an FTA VAT audit?

Frequent triggers for an FTA audit include substantial VAT refund claims, inconsistent data between VAT returns and Corporate Tax declarations, and repeated late filings. The FTA’s AI-driven systems also flag businesses with unusual transaction patterns or those operating in high-risk sectors. Maintaining precise internal records and performing regular health checks are the most effective ways to ensure your enterprise remains resilient during these comprehensive formal reviews.

How long must UAE businesses keep their VAT records?

UAE businesses are required to retain their VAT records for a minimum period of five years following the end of the tax period to which they relate. For entities involved in real estate transactions, this mandatory retention period is extended to 15 years. These records must be readily accessible in a digital or physical format and must be provided in Arabic if specifically requested by the authority during a formal inspection.

What is the difference between zero-rated and exempt supplies for VAT recovery?

The primary distinction lies in the right to recover input tax. Zero-rated supplies are taxable at 0%, which entitles the business to reclaim VAT on related expenses incurred for those supplies. Exempt supplies aren’t subject to VAT, but they don’t allow for any input tax recovery. Misunderstanding this distinction is a frequent source of technical error, often leading to the incorrect recovery of tax that must later be repaid with interest.

Do I need a tax agent to file my VAT return in the UAE?

While the law doesn’t mandate the appointment of a registered tax agent to file returns, many enterprises engage expert oversight to navigate the complexities of the UAE tax landscape. Managing the nuances of the Reverse Charge Mechanism and ensuring precise revenue classification requires technical proficiency that goes beyond basic bookkeeping. Partnering with a specialist ensures that your filings are accurate and compliant, significantly reducing the risk of administrative penalties.

Can I claim VAT on business lunch expenses for clients?

You generally cannot recover VAT on business lunch expenses provided to clients or non-employees. Under the UAE Executive Regulations, entertainment services are classified as non-recoverable, even if they’re incurred for legitimate business purposes. Claiming these costs is one of the common VAT filing mistakes in the UAE businesses make, as the FTA strictly enforces the ‘blocked’ status of hospitality and entertainment expenditures during their routine digital audits.